Real GDP

Since the Great Financial Crisis (GFC), forecasters have tended to be over-optimistic in their real GDP forecasts. That was true again in 2015. In the twelve major economies tracked in this blog, real GDP growth fell short of forecasters' expectations in ten and exceeded expectations in just two economies. The weighted average forecast error for 2015 was -0.46 percentage points, almost twice as large as the 2014 error.

Based on current estimates, 2015 real GDP growth for the US and fell short of the December 2014 consensus by 0.5 pct pts. The biggest downside misses were for Brazil (-4.6 pct pts), Russia (-2.7), Canada (-1.2), Korea (-1.1), Australia (-0.8), and Mexico (-0.8%). India beat forecasts by 1.1 pct pts. On balance, it was a fifth consecutive year of global growth trailing expectations.

CPI Inflation

Inflation forecasts for 2015 were seriously too high. Ten of the twelve economies are on track for significantly lower than forecast inflation, while inflation will be higher than expected in two countries. The weighted average forecast error for the 12 countries was a massive 1.7 pct pts.

The biggest downside misses on inflation were in China (-3.6 pct pts), Korea (-2.7), Mexico (-2.5%), India (-2.4), the UK (-2.3), the US (-1.9%) and Japan (-1.9%). The biggest upside misses on inflation were in countries that experienced large currency depreciations, including Russia (+5.8) and Brazil (+3.3).

Policy Rates

Economists forecasts of central bank policy rates for the end of 2015 anticipated too much tightening by DM central banks and too little easing for most EM central banks.

In the DM, the Fed, the Bank of England failed to tighten as much as expected. The Reserve Bank of Australia and the Bank of Canada, which were also expected to tighten, unexpectedly cut their policy rates. In the EM, the picture was more mixed. In China and India, where inflation fell more than expected, the central banks eased more aggressively than expected. In Russia and Brazil, where inflation was much higher than expected, Russia's central bank eased less than expected and Brazil's central bank was forced to tighten much more than expected.

10-year Bond Yields

In nine of the twelve economies, 10-year bond yield forecasts made one year ago were too high. Weaker than expected growth and inflation in most countries pulled 10-year yields down almost everywhere compared with forecasts of rising yields made a year ago.

In all of the DM economies we track, 10-year bond yields surprised strategists to the downside. The weighted average DM forecast error was -0.54 percentage points. The biggest misses were in Canada (-1.01 pct. pt.), the UK (-0.90) and the US (-0.85). In the EM, bond yields were lower than forecast where inflation fell in China, Korea and Mexico, but much higher than expected where inflation rose sharply in Brazil and Russia.

Exchange Rates

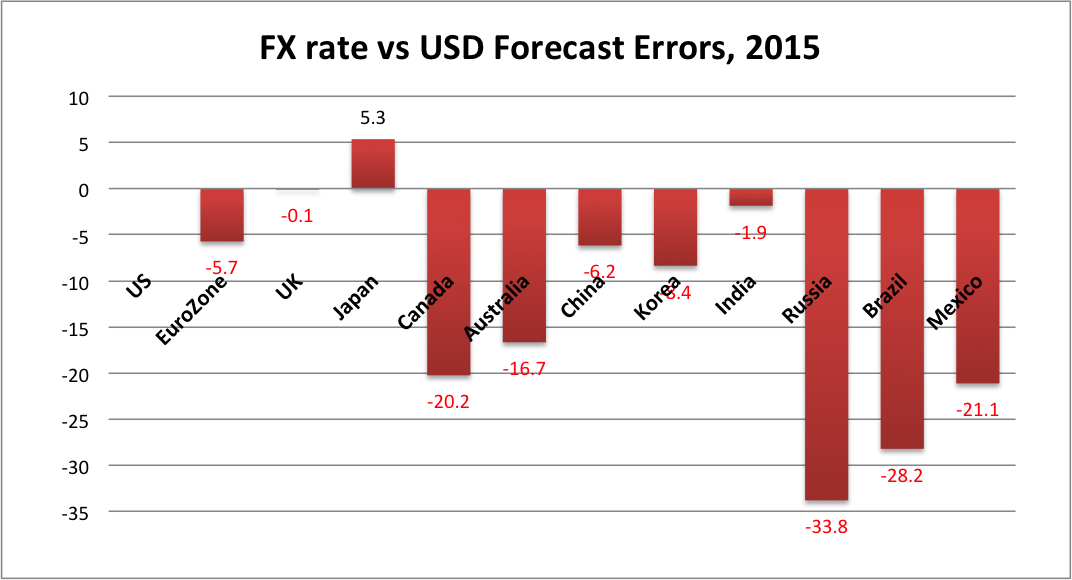

The strength of the US dollar once again surprised forecasters. The USD was expected to strengthen against most currencies, but not by nearly as much as it did. On a weighted average basis, the 11 currencies depreciated versus the USD by about 8.1% more than forecast a year ago.

The USD was expected to strengthen because many forecasters believed the Fed would begin to tighten around mid-2015. While the Fed had been promising to tighten this year, it found various reasons to delay, with the first tightening finally occurring on December 16. If everything else had been as expected, the Fed's delay would have tended to weaken the USD. But everything else was far from as expected. Most other central banks eased policy by more than expected. In addition, oil and other commodity prices weakened more than expected so that commodity currencies like RUB, MXN, CAD and AUD weakened much more than forecast.

The biggest FX forecast miss was, not surprisingly, the RUB, more than 30 percentage points weaker than forecast a year ago. Other big misses were for BRL (-28.2 pct pts), MXN (-21.1), CAD (-20.2) and AUD (-16.7). JPY was the only currency that depreciated less than forecast versus the USD.

North American Stock Markets

A year ago, equity strategists were cautiously optimistic that North American stock markets would turn in a solid, if unspectacular, performance in 2015. However, in a year when the major global macro surprises were weaker than expected real GDP growth and much lower than expected inflation reflecting sharp declines in commodity prices, equity performance failed to live up to forecasts. I could only compile consensus equity market forecasts for the US and Canada. News outlets gather such year end forecasts from the high profile US strategists and Canadian bank-owned dealers. As shown below, those forecasts called for a 7.5% gain in the S&P500 and a 6.2% rise in the S&PTSX Composite.

As of December 18, 2015, the S&P500 was down 3.9% (not including dividends) for an error of -11.4 percentage points. The S&PTSX300, battered by the drop in oil and other commodity prices, was down 11.0% for an error of -17.2 percentage points.

Globally, actual stock market performance was mixed on a year-to-date basis as of December 18, 2015. Stocks performed relatively well in the Eurozone and Japan, where quantitative easing continued and monetary policy became even more accommodative. China and Korea also saw gains, although both markets are well off the double digit gains seen prior to China's August equity market rout. The US and UK, where central banks tilted toward tightening monetary policy, posted losses. Brazil, Canada, Australia and Russia suffered losses inflicted by the drop in commodity prices.

Investment Implications

While the 2015 global macro forecast misses were similar in direction and larger in magnitude relative to those of 2014, the investment implications were somewhat different. Global nominal GDP growth was once again much weaker than expected, reflecting downside forecast errors on both global real GDP growth and global inflation. In 2014, this negative development for equities was more than offset by easier than expected global monetary policy, as US and other DM equity markets performed well. In 2015, most global central banks either tightened less than expected or eased more than expected, but with the Fed signalling tightening for most of the year, weaker nominal GDP growth and the strong US dollar held the US equity market to a modest decline. In Japan and the Eurozone, where central banks continued to ease, equities outperformed. In Canada, Australia, Mexico and Russia, falling commodity prices put downward pressure on equity markets.

Similar to 2014, the downside misses on growth and inflation and the central banks easing in most countries resulted in a modest positive returns on DM government bonds in 2015, and significant outperformance of 10-year government bonds versus equities in the US, UK and Canada.

Divergences in growth, inflation and central bank responses, along with the sharp declines in crude oil and other commodity prices, again led to much larger currency depreciations versus the USD than forecast. For Canadian investors, this meant that investments in both equities and government bonds denominated in US dollars, Japanese Yen and UK Sterling, leaving the currency exposure unhedged, were winners. Big losers were Canadian and EM equities, commodities, and EM bonds denominated in local currencies.

As 2016 economic and financial market forecasts are rolled out, it is worth reflecting that such forecasts form a very uncertain basis for year-ahead investment strategies. The best performing portfolios for Canadian investors in recent years have tended to be those that are well diversified, risk-balanced and currency unhedged.

No comments:

Post a Comment