It's now time of year to look ahead to global macro prospects for 2016. I have posted similar outlooks for the past two years (here and here) and followed up at the end of each year with an assessment of those forecasts (here and here). I will state again why I find this exercise useful. I assemble consensus views on global growth, inflation, interest rate and exchange rate outlooks not because I have faith in forecasts. I do it because the consensus view on the year ahead is presumably already built into market prices. The consensus view, as Howard Marks says, is "what 'everyone knows' and is usually unhelpful at best and wrong at worst". What will move markets in 2016 is not the current consensus forecast, but the ways in which actual economic developments diverge from that consensus.

With the foregoing caveat in mind, here, in a nutshell, is what the consensus view is telling us about 2016:

- global real GDP growth is expected to be stronger than 2015;

- global inflation is expected to be higher than in 2015;

- The Fed is expected to hike the Fed Funds rate by 50 or maybe 75 basis points and central banks in the UK and Mexico are also expected to tighten at least once;

- The Eurozone, Japan and Canada are all expected to leave their policy rates unchanged, while one 25 bp rate cut is expected in China, India, Australia and Korea;

- In the DM, 10-year government bond yields are expected to rise in all of the economies we track except Australia; In the EM, yields are expected to rise modestly in China, Korea and Mexico, but to fall in India, Russia and Brazil.

- After strengthening against all the currencies we track in 2015, the US dollar is expected to turn in a more mixed performance. USD is expected to strengthen further against EUR, AUD, CNY, KRW, INR and BRL. However, by the end of 2016, the USD is expected to be weaker against JPY, GBP, CAD, and RUB.

- After poor performances in 2015, equity strategists tell us that US and Canadian stock markets are expected to post gains of about 5.5% and 10%, respectively.

If these consensus forecasts sound familiar, thats because they are very similar to forecasts made at the end of 2013 and the end of 2014. Each year, global growth was expected to pick up, global inflation was expected to move higher, the Fed was expected to lead global tightening, bond yields were expected to rise and North American stocks were expected to rally. Both 2014 and 2015 witnessed big macro forecast misses by the consensus. These misses were characterized by weaker than expected global real GDP growth and inflation, lower than expected bond yields, greater than expected USD strength and weaker than expected stock price gains. Are we being set up for similar forecast misses in 2016 or will this be the year when the consensus is correct and things turn around?

Global Real GDP Growth Forecasts

Last year at this time, global growth was expected by the IMF to pick up to 3.8% in 2015 while global commercial bank economists expected a more modest acceleration to 3.4%. Instead, 2015 global growth is now estimated to have slowed to 3.1%.

This year, forecasters tell us once again that global growth will pick up in 2016 to 3.6% (IMF October forecast), or to 4.0% (OECD December forecast), or to 3.4% (average of global commercial bank forecasts).

2016 real GDP growth is expected to be stronger almost everywhere, but with the notable exceptions of the US and China. Economies with the largest consensus forecast growth pickup include Canada (1.9% in 2016 vs 1.2% in 2015), Mexico (3.0% vs 2.5%), Japan (1.1% vs 0.7%), India (7.8% vs 7.4%), Australia (2.6% vs 2.3%), and Eurozone (1.8% vs 1.5%).

While global growth is expected to be a bit stronger in 2016, the divergence between DM and EM growth performance is expected to continue. EM growth is consistently higher than DM growth, but the important divergence is that, for a third consecutive year, DM economies are expected to grow at or above their trend (or potential) rate of growth, while most EM economies are expected to grow below their trend rate. In the chart below, the blue bars show the 2016 consensus growth forecast versus the OECD estimate of the trend growth rate for each economy.

In 2016, the larger DM economies are expected to grow at an above trend pace, while Canada and Australia and are expected to grow at trend. In contrast, three of the larger EM economies are expected to grow well below trend: Brazil (3.4% below trend), Russia (1.5% below trend) and China (0.4% below trend).

In the chart above, the red bars show the latest OECD composite leading indicators (CLIs) versus trend for each of the economies. As was the case a year ago, these CLIs generally support weaker 2016 growth than economists are forecasting, with a few exceptions.

In the DM economies, the leading indicators suggest that growth could surprise on the downside, especially in US, UK, Japan and Canada. In the EM economies, CLIs suggest that growth could be weaker than expected in China, India and Mexico, but stronger than expected, although still below trend, in Brazil and Russia.

Global Inflation Forecasts

Global inflation has consistently fallen short of expectations since 2013. This has occurred in spite of unprecedented efforts by central banks to fight disinflation.

A year ago, global inflation for the entire set of world economies was expected by the IMF to edge up to 3.8% by the end of 2015 from 3.7% at the end of 2014. By October 2015, the IMF had cut its year-end 2015 global inflation forecast to 3.5%. Meanwhile, a year ago, global commercial bank economists expected weighted average inflation for 12 major economies we track to move up to 2.8% in 4Q15 from 2.1% in 4Q14. These same economists now expect that weighted average inflation for these countries fell to 2.0% in 4Q15. For 2016, the global commercial bank economists forecast that weighted average inflation for the 12 countries will rise to 2.3% in 4Q16. The OECD expects an even bigger acceleration fore the 12 countries to 2.5%.

These forecasts, many of them made between early October and early-December, may already subject to downward revision. Crude oil prices ranged from $43 to $51 per barrel during the period these forecasts were made with expectations that prices would firm further heading into 2016. Instead, in the wake of the December OPEC meeting, the price has fallen to $36/bbl in late December and looks likely to remain depressed for a considerable period of time.

In most countries, inflation can be expected to remain weak. Considerable slack remains in the global economy, especially in EM economies. Wage growth remains subdued. Commodity prices are likely to remain weak. Inflation expectations are stable and soft.

Other Non-Consensus Views

Some economists, who are not part of the consensus, have a much darker view of 2016 prospects. One such economist is David Levy, of the Jerome Levy Forecasting Centre, which has a long and enviable forecasting track record.

In a recent interview with Barron's, Levy made the following highly contrarian statements:

Levy: [T]here is no way the U.S. by itself is about to keel over. The danger is not so much that we’re going to start to slide sharply, but rather that conditions overseas will become much rockier.

Barrons: Which could pull the U.S. into a recession?

Levy: Yes, and there are several reasons why. Such a scenario has never happened, certainly not in modern history. There is no postwar recession prior to which the U.S. economy was doing fine, only to get knocked down by the rest of the world. That’s one reason people don’t see the risk. But the emerging markets are not just going into a recession, they are going through a secular adjustment. .... We expect not only a global recession, but also general asset deflation, aggravated by the fact that there is no room to cut interest rates at the major central banks.... Bit by bit, the global economy is falling into recession, with the U.S. bringing up the rear. ...We expect that the Fed will reverse course later next year. In all probability, the slowly spreading global recession will intensify and ultimately engulf the entire planet. It’s at least 2 to 1 that we’ll be in a recession at the end of 2016.

Levy is not alone in warning that 2016 could fall well short of consensus forecasts. Albert Edwards at SocGen, Niall Ferguson of Harvard, Russell Napier, and Lakshman Achuthan of ECRI are also warning of the likelihood of weaker growth or recession.

I'm not suggesting that we should toss the consensus forecast in the trash and use Levy's quite plausible forecast as a base case. But I am suggesting that we should apply a hefty discount rate to the consensus and consider the risks around the benign outcome that reflects "what everybody knows".

Conclusions and Questions

2015 turned out to be a third consecutive year in which global growth was modestly disappointing, but the real story for markets was the divergences in real GDP growth. Will the divergences of 2014-15 continue? If so, the US Fed will likely be joined by the Bank of England and perhaps a few other central banks in tightening monetary policy in 2016, while the ECB, BoJ and PBoC will likely maintain their current accommodative policies or ease further. In this scenario, the US$ is likely to continue to appreciate against currencies of countries whose central banks remain accommodative. Further appreciation of the US dollar combined with below trend growth in China, Brazil and Russia will, barring a major geopolitical event, wii likely continue to weigh on commodity prices and the currencies of commodity exporting countries.

The questions one should ask about 2016 consensus forecasts are the same as we asked a year ago:

- Can the macro divergences between above-trend growth in some key DM economies and below-trend growth in key EM economies be sustained without serious financial instability in some countries and significant volatility in global currency and financial markets?

- Can commodity prices stabilize and recover even as the USD continues to rally and global commodity supply continues to outpace global demand.

- Can China and other EM economies prevent hard landings for their over-leveraged economies?

- Can Canada and Australia, with overheated housing markets, rebound to grow at or above trend after a sharp fall in commodity prices and as the Fed continues to raise its policy rate?

- Will we look back on 2016 as yet another year that started with optimistic forecasts and ended with disappointment?

A year ago, my answers to these questions were: No, No, Don't Know, Unlikely, and Probably. I can see little reason to change these answers as we head into 2016. In the near future, I will turn to the question of how Canadian investors should think about 2016 as another year with macro risks skewed to the downside.

Ted Carmichael is Founding Partner of Ted Carmichael Global Macro. Previously, he held positions as Chief Canadian Economist with JP Morgan Canada and Managing Director, Global Macro Portfolio, OMERS Capital Markets.

It is time to review how the macro consensus forecasts for 2015 that were made a year ago fared. It's not only interesting to look back at the notable global macro misses and the biggest forecast errors of the past year, it also helps us to understand 2015 investment returns.

Real GDP

Since the Great Financial Crisis (GFC), forecasters have tended to be over-optimistic in their real GDP forecasts. That was true again in 2015. In the twelve major economies tracked in this blog, real GDP growth fell short of forecasters' expectations in ten and exceeded expectations in just two economies. The weighted average forecast error for 2015 was -0.46 percentage points, almost twice as large as the 2014 error.

Based on current estimates, 2015 real GDP growth for the US and fell short of the December 2014 consensus by 0.5 pct pts. The biggest downside misses were for Brazil (-4.6 pct pts), Russia (-2.7), Canada (-1.2), Korea (-1.1), Australia (-0.8), and Mexico (-0.8%). India beat forecasts by 1.1 pct pts. On balance, it was a fifth consecutive year of global growth trailing expectations.

CPI Inflation

Inflation forecasts for 2015 were seriously too high. Ten of the twelve economies are on track for significantly lower than forecast inflation, while inflation will be higher than expected in two countries. The weighted average forecast error for the 12 countries was a massive 1.7 pct pts.

The biggest downside misses on inflation were in China (-3.6 pct pts), Korea (-2.7), Mexico (-2.5%), India (-2.4), the UK (-2.3), the US (-1.9%) and Japan (-1.9%). The biggest upside misses on inflation were in countries that experienced large currency depreciations, including Russia (+5.8) and Brazil (+3.3).

Policy Rates

Economists forecasts of central bank policy rates for the end of 2015 anticipated too much tightening by DM central banks and too little easing for most EM central banks.

In the DM, the Fed, the Bank of England failed to tighten as much as expected. The Reserve Bank of Australia and the Bank of Canada, which were also expected to tighten, unexpectedly cut their policy rates. In the EM, the picture was more mixed. In China and India, where inflation fell more than expected, the central banks eased more aggressively than expected. In Russia and Brazil, where inflation was much higher than expected, Russia's central bank eased less than expected and Brazil's central bank was forced to tighten much more than expected.

10-year Bond Yields

In nine of the twelve economies, 10-year bond yield forecasts made one year ago were too high. Weaker than expected growth and inflation in most countries pulled 10-year yields down almost everywhere compared with forecasts of rising yields made a year ago.

In all of the DM economies we track, 10-year bond yields surprised strategists to the downside. The weighted average DM forecast error was -0.54 percentage points. The biggest misses were in Canada (-1.01 pct. pt.), the UK (-0.90) and the US (-0.85). In the EM, bond yields were lower than forecast where inflation fell in China, Korea and Mexico, but much higher than expected where inflation rose sharply in Brazil and Russia.

Exchange Rates

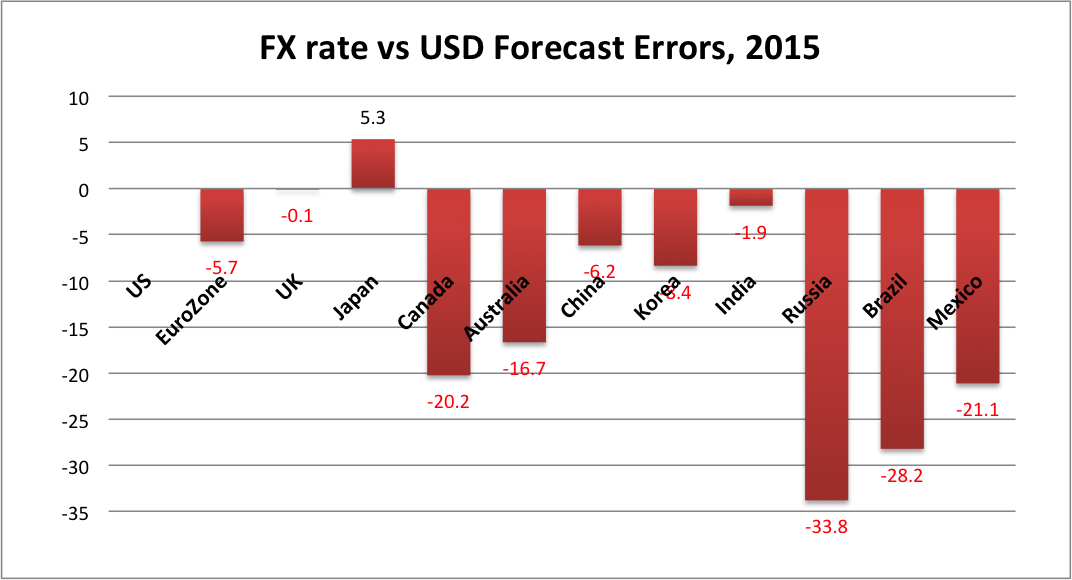

The strength of the US dollar once again surprised forecasters. The USD was expected to strengthen against most currencies, but not by nearly as much as it did. On a weighted average basis, the 11 currencies depreciated versus the USD by about 8.1% more than forecast a year ago.

The USD was expected to strengthen because many forecasters believed the Fed would begin to tighten around mid-2015. While the Fed had been promising to tighten this year, it found various reasons to delay, with the first tightening finally occurring on December 16. If everything else had been as expected, the Fed's delay would have tended to weaken the USD. But everything else was far from as expected. Most other central banks eased policy by more than expected. In addition, oil and other commodity prices weakened more than expected so that commodity currencies like RUB, MXN, CAD and AUD weakened much more than forecast.

The biggest FX forecast miss was, not surprisingly, the RUB, more than 30 percentage points weaker than forecast a year ago. Other big misses were for BRL (-28.2 pct pts), MXN (-21.1), CAD (-20.2) and AUD (-16.7). JPY was the only currency that depreciated less than forecast versus the USD.

North American Stock Markets

A year ago, equity strategists were cautiously optimistic that North American stock markets would turn in a solid, if unspectacular, performance in 2015. However, in a year when the major global macro surprises were weaker than expected real GDP growth and much lower than expected inflation reflecting sharp declines in commodity prices, equity performance failed to live up to forecasts. I could only compile consensus equity market forecasts for the US and Canada. News outlets gather such year end forecasts from the high profile US strategists and Canadian bank-owned dealers. As shown below, those forecasts called for a 7.5% gain in the S&P500 and a 6.2% rise in the S&PTSX Composite.

As of December 18, 2015, the S&P500 was down 3.9% (not including dividends) for an error of -11.4 percentage points. The S&PTSX300, battered by the drop in oil and other commodity prices, was down 11.0% for an error of -17.2 percentage points.

Globally, actual stock market performance was mixed on a year-to-date basis as of December 18, 2015. Stocks performed relatively well in the Eurozone and Japan, where quantitative easing continued and monetary policy became even more accommodative. China and Korea also saw gains, although both markets are well off the double digit gains seen prior to China's August equity market rout. The US and UK, where central banks tilted toward tightening monetary policy, posted losses. Brazil, Canada, Australia and Russia suffered losses inflicted by the drop in commodity prices.

Investment Implications

While the 2015 global macro forecast misses were similar in direction and larger in magnitude relative to those of 2014, the investment implications were somewhat different. Global nominal GDP growth was once again much weaker than expected, reflecting downside forecast errors on both global real GDP growth and global inflation. In 2014, this negative development for equities was more than offset by easier than expected global monetary policy, as US and other DM equity markets performed well. In 2015, most global central banks either tightened less than expected or eased more than expected, but with the Fed signalling tightening for most of the year, weaker nominal GDP growth and the strong US dollar held the US equity market to a modest decline. In Japan and the Eurozone, where central banks continued to ease, equities outperformed. In Canada, Australia, Mexico and Russia, falling commodity prices put downward pressure on equity markets.

Similar to 2014, the downside misses on growth and inflation and the central banks easing in most countries resulted in a modest positive returns on DM government bonds in 2015, and significant outperformance of 10-year government bonds versus equities in the US, UK and Canada.

Divergences in growth, inflation and central bank responses, along with the sharp declines in crude oil and other commodity prices, again led to much larger currency depreciations versus the USD than forecast. For Canadian investors, this meant that investments in both equities and government bonds denominated in US dollars, Japanese Yen and UK Sterling, leaving the currency exposure unhedged, were winners. Big losers were Canadian and EM equities, commodities, and EM bonds denominated in local currencies.

As 2016 economic and financial market forecasts are rolled out, it is worth reflecting that such forecasts form a very uncertain basis for year-ahead investment strategies. The best performing portfolios for Canadian investors in recent years have tended to be those that are well diversified, risk-balanced and currency unhedged.

At the risk of sounding like a broken record, I am going to write again about whether Canada is, was or will be experiencing a recession.

You may wonder why I am doing this. After all, on December 1 the authoritative Peter Mansbridge, anchor of the CBC National news pronounced that the recession is "officially over", citing the report from Statistics Canada that real GDP grew 0.6% (or 2.3% at an annual rate) in 3Q15 after contracting modestly in the previous two quarters. According to this interpretation, the so-called "technical recession" meaning two (or more) consecutive quarters of negative real GDP growth, a definition widely adopted by the general media and the business press, was over.

However, I have recently joined the C.D. Howe Institute's Business Cycle Committee (BCC), which is described on the Institute's web site as "an arbiter of business cycle dates in Canada.... The Council performs a similar function to the National Bureau of Economic Research (NBER) Business Cycle Dating Committee in the United States."

This is a big responsibility and one that I take very seriously. When I told my wife about it, she was puzzled, and asked why I would want to spend my time on such an activity. She correctly pointed out that most people are more interested in what will happen in the future than in having precise dates upon which the economy entered into and exited from recessions. I explained that economists can do a better job giving guidance about the future direction of the economy if they understand the causes and dynamics of past business cycles.

I was not a member of the BCC when it issued its latest report, which concluded that "as of July 22, data did not provide evidence that Canada had entered an economic downturn", but said it would review its position later in 2015.

What is a Recession?

In a background Commentary to the first report of the Business Council Committee, Philip Cross and Phillipe Bergevin defined a recession as follows:

A recession is the phase of the business cycle when aggregate economic activity is contracting.... The drop in economic activity is a self-reinforcing process, where lower incomes lead to cuts in spending, which trigger declines in output and possibly employment, which lead to further reductions in incomes.

The Commentary goes on to cite the NBER definition of recession:

A significant decline in activity spread across the economy, lasting more than a few months, visible in industrial production, employment, real income, and wholesale-retail trade.

What these definitions have in common is that they require a "significant" contraction of economic activity, measured in four key dimensions: real output, employment, real income, and real spending or sales. To qualify as "significant", a contraction must meet the 3 P's test: it must be pronounced, pervasive, and persistent. To be pronounced, the contraction must show some depth or amplitude. To be pervasive, it must demonstrate some duration or length. To be persistent, it must show scope or breadth across the key dimensions of output, employment, real income and spending.

Cross and Bergevin note that there is an element of professional judgement in dating recessions:

Although one can use these considerations as guides in identifying and dating recessions, it is worth emphasizing that it is impractical to establish preset conditions with respect to amplitude, duration, and scope because these considerations need to be judged simultaneously and because the economy and its measurement change over time. Thus, the [business cycle] chronology we present ... is the result of a careful balancing of these different considerations.

It should be clear from this discussion that Peter Mansbridge and other media commentators were not referring to any rigorous definition of recession when they pronounced that the recession is "officially over". Indeed, it may not yet be possible to determine whether a recession "officially began" sometime in the first half of 2015, because professional judgement has not yet been made on whether it was pronounced, pervasive and persistent enough to qualify as a recession.

Toward a Made-in-Canada Definition of Recession

In the excellent work on dating recessions back to 1926 done so far by the C.D. Howe Institute's Business Cycle Council, I have one fundamental problem. Of the four key dimensions of economic activity that are key to dating a recession, the BCC has only analyzed two: real output and employment.

The reason for this seems to be that Canada lacks monthly data on real sales and real income. In the United States, the NBER does not give any significant weight to quarterly real GDP in dating recessions. It relies on monthly data for industrial production, non-farm business payrolls, real personal income, and real manufacturing and trade sales.

In Canada, we have monthly data on real GDP for both the private and public sectors and monthly data on employment by industry. Statistics Canada does not produce monthly data for real income or for real sales.

This raises two questions for me.

First, are we attempting the measure and date the "business cycle" or some broader measure of the "economic cycle" comprising both the private business sector and the public sector?

It is well known that the business sector is more cyclical than the broad economy which includes the public sector. I believe that it is the business sector that is most prone to cyclical dynamics and that this should be the focus of dating business cycles rather than the total economy. That means we should focus on measures of private sector output and employment, not measures of total real GDP and total employment. Thus, it would be possible to have a business cycle recession without experiencing a significant decline in total real output or employment.

Second, in the absence of monthly data for real income, should we not include a focus on quarterly real income measures, which Statistics Canada does produce? The quarterly national income and expenditure accounts provides both measures of output, real gross domestic product (GDP) and real gross domestic income (GDI). Using measures of real income from the quarterly national accounts allows us to move toward a "made-in-Canada" definition of the business cycle.

Canada's economy is different from the US economy. Canada is a smaller, more trade dependent and more resource dependent economy than is the United States. This means that Canada's prosperity is more dependent on movements in the terms of trade (the price of its exports relative to its imports) and the exchange rate. The effects of these movements can introduce quite different behaviour in real GDI than in real GDP. As I have argued in a previous post, looking only at real output, measured by real GDP, often misses the point, especially when there are large movements in the terms of trade and the exchange rate, as has been the case in 2014-15.

A brilliant exposition of this thinking is contained in a Statistics Canada publication which I just recently stumbled upon. The 2012 study, "Natural Resources, the Terms of Trade, and Real Income Growth in Canada: 1870 to 2010", by John R. Baldwin and Ryan Macdonald, provides a rich account of the historical development of Canada's natural resources. In addition, using annual data, it measures the contributions to real income growth arising from real output growth, terms of trade shifts and exchange rate movements. It demonstrated that over the 140 year period, real income grew substantially more than real output because over that long period of time, terms of trade and real exchange rate effects added to real income growth.

Recent changes to the presentation of the quarterly national income and expenditure accounts make the same information available on a quarterly basis back to 1981. It seems feasible that such quarterly data could be calculated at least back to 1946.

The chart below shows drawdowns from quarterly peaks in real GDP and real GDI since 1981. The drawdown is the cumulative % decline from the previous peak level.

In recent recessions, in 2000-01 and 2008-09, notice that the cumulative declines in real GDI were both larger and more protracted than the declines in real GDP. This is because, the price of commodities produced in Canada fell quite sharply and the terms of trade weakened significantly. In the most recent period, real GDP fell only modestly, by just a cumulative 0.24% over the first and second quarters of 2015, but real GDI, fell for the three consecutive quarters to 3Q15 and by a much larger 1.5%. Since the terms of trade are continuing to decline in 4Q15, this story is still unfolding and it is possible that the downturn in real GDI could deepen further.

I believe that this evidence tips the scales in favour of judging that the 2015 downturn meets the 3 P's test:

- it is pronounced, particularly in the depth of decline of real GDI;

- it is pervasive, in that monthly real GDP, monthly real manufacturing and trade sales, and quarterly real GDI all experienced declines, only employment did not (so far); and

- it is persistent, in that quarterly GDI declined for three consecutive quarters, monthly GDP declined for six of the nine months months from January through September and remained well below the December 2014 peak level.

For this reason, I believe that, based on current evidence, a recession probably did begin in early 2015. I also think that it was a more serious recession than indicated by the decline in real GDP. However, I do not believe that a definitive conclusion can yet be reached on dating the beginning and the end of the recession. Unfortunately, this nuanced conclusion is unlikely to ever be reported by Peter Mansbridge on The National.